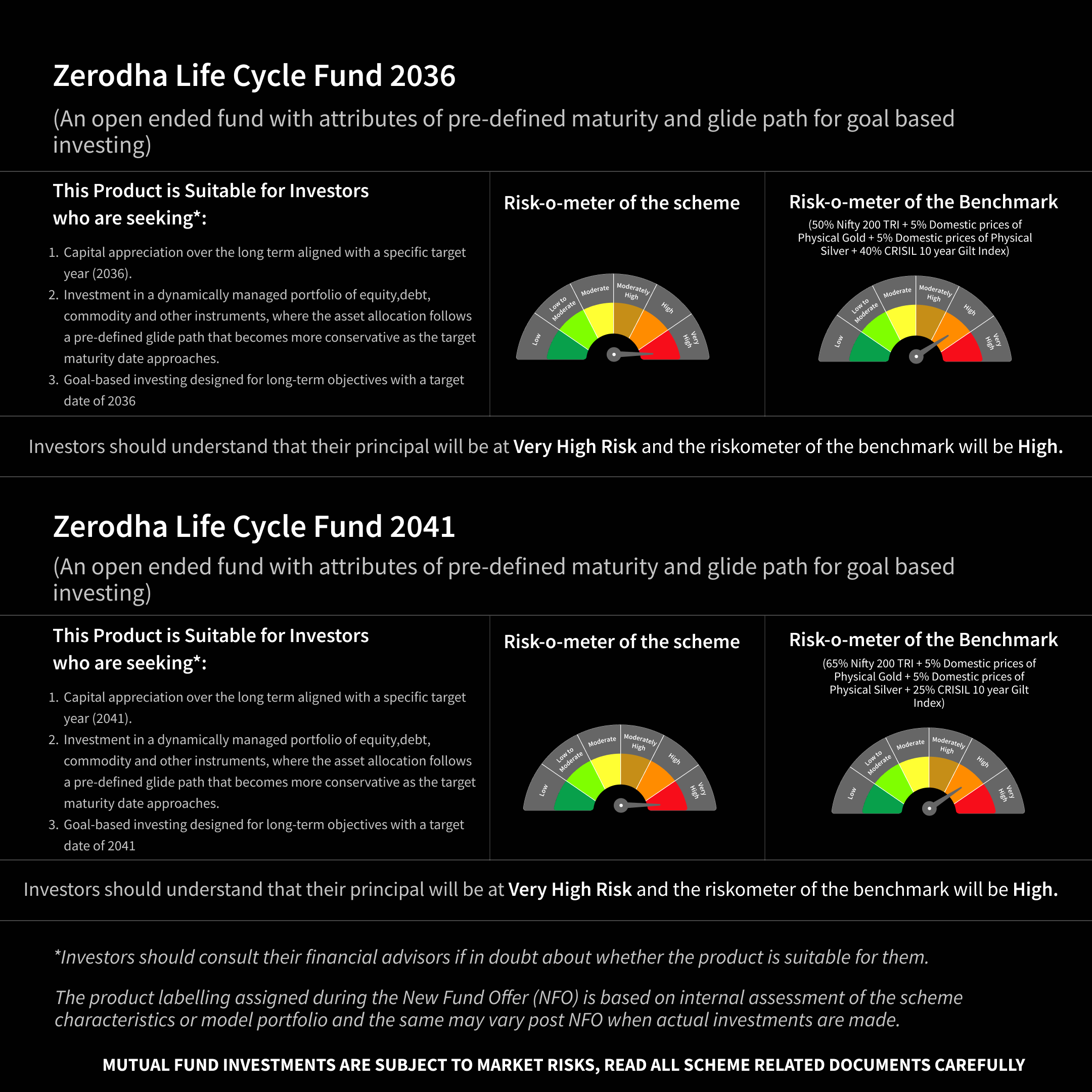

Zerodha Life Cycle Funds: Automated Target-Date Investing for Your Goals

Most people invest with a finish line in mind, whether that's retirement, a child's higher education, a home down payment, or a car a few years out. The hard part isn't picking the goal. It's that the right asset allocation for that goal keeps changing as the finish line gets closer. A portfolio that makes sense 15 years away from a goal looks nothing like one that makes sense 2 years away. Managing that shift manually, year after year, is where most goal-based plans might fall apart.

This is the gap that lifecycle funds, also called target date funds or target maturity funds, are built to close. They are goal-based mutual funds that follow a pre-defined glide path, automatically moving your money from growth-oriented assets toward conservative ones as your target year approaches, with no annual rebalancing on your part. It is, in the simplest terms, a mutual fund with a finish line.

Zerodha Fund House has launched India's first target date mutual funds built on this idea: the Zerodha Life Cycle Funds.

Give a date to your goals and let the fund handle the rest.

What is a Target Date Fund?

A target date fund is a single mutual fund organized around a specific maturity year, the "target year". You pick the fund whose year lines up with your goal, for example a fund for retirement in 2041 or a fund for your child's education in 2036, and the fund manages the asset allocation journey for you.

Globally, target date funds are one of the most widely adopted ways to save for long-term goals, especially retirement. The category has grown into a market managing over $4 trillion in assets, largely on the back of US retirement plans where these funds are a default investment option. The Zerodha Life Cycle Funds bring that same do-it-for-me, set-and-forget approach to Indian investors for the first time.

What are Zerodha Life Cycle Funds?

Zerodha Life Cycle Funds are open-ended mutual funds structured around a target maturity year. This rule-based series launches with two maturity variants:

- Zerodha Life Cycle Fund 2036, maturing in roughly 10 years

- Zerodha Life Cycle Fund 2041, maturing in roughly 15 years

More maturity variants are in the pipeline, so investors will eventually be able to match a fund closely to whatever year their goal falls in.

Each fund carries its target year right in the name, which makes the choice intuitive. Investing for a goal that is 15 years away? Pick the fund whose maturity year is closest to that horizon. That's the whole decision.

How do Zerodha Life Cycle funds work?

The engine inside every Zerodha Life Cycle Fund is its glide path: a pre-defined schedule that gradually shifts the portfolio's asset allocation over time, without any ongoing intervention from you. This is how a glide path reduces risk as you near your goal.

Early years (Growth-Oriented phase) When the target year is far away, the fund runs a growth-oriented, higher-risk allocation. On the equity side it tracks the Nifty LargeMidcap 250 index, combined with allocations to arbitrage and to commodities like gold and silver for diversification across asset classes.

Approaching maturity (Conservative phase) As the target year draws closer, the fund systematically trims equity exposure and increases allocation to more conservative instruments such as Indian government securities (G-secs) and other debt.

Crucially, this is a gradual transition rather than a sudden switch. The allocation changes are smooth, systematic, and rule-based, which is what separates a true glide path from simply trying to time the move from equity to debt yourself. This is horizon-based asset allocation handled automatically by a single fund.

Asset Allocation for Zerodha Life Cycle Fund Series

Here's the allocation schedule proposed to be followed for both the 2036 and 2041 maturity variants, year by year as per the asset allocation defined in the scheme document:

10 Year tenure (e.g. Zerodha Life Cycle Fund 2036)*

| Year | EquityNifty Large Midcap 250 Index | CommoditiesGold & Silver ETFs | DebtGovernment Securities | Arbitrage |

|---|---|---|---|---|

| 2026 to 2031 | 50% to 65% | 0% to 10% | 10% to 20% | 10% to 20% |

| 2031 to 2033 | 35% to 50% | 0% to 10% | 25% to 30% | 20% to 35% |

| 2033 to 2035 | 20% to 30% | 0% to 10% | 25% to 30% | 35% to 45% |

| Maturity year | 10% to 20% | 0% to 10% | 25% to 30% | Up to 50% |

15 Year tenure (e.g. Zerodha Life Cycle Fund 2041)*

| Year | EquityNifty Large Midcap 250 Index | CommoditiesGold & Silver ETFs | DebtGovernment Securities | Arbitrage |

|---|---|---|---|---|

| 2026 to 2031 | 70% to 80% | 0% to 10% | 10% to 20% | 0% |

| 2031 to 2036 | 50% to 65% | 0% to 10% | 10% to 20% | 10% to 20% |

| 2036 to 2038 | 35% to 50% | 0% to 10% | 25% to 30% | 20% to 35% |

| 2038 to 2040 | 20% to 30% | 0% to 10% | 25% to 30% | 35% to 45% |

| Maturity year | 10% to 20% | 0% to 10% | 25% to 30% | Up to 50% |

As the table shows, a fund for financial goals in 2036 starts meaningfully more conservative than a 2041 fund today, simply because it has less runway. Both then converge toward a conservative stance in their final years.

Asset Allocation For All Life Cycle Fund Tenures

SEBI has specified the exact asset allocation ranges for each phase of each Life Cycle Fund tenure. Here's a complete look:

Life Cycle Fund - 5 Year Tenure

| Years to maturity | Equity (%) | Debt (%) | Gold/Silver ETFs / ETCDs / InvITs (%) |

|---|---|---|---|

| 3–5 years | 35–50% | 25–50% | 0–10% |

| 1–3 years | 20–35% | 25–65% | 0–10% |

| < 1 year | 5–20% | 25–65% | 0–10% |

Life Cycle Fund - 10 Year Tenure

| Years to maturity | Equity (%) | Debt (%) | Gold/Silver ETFs / ETCDs / InvITs (%) |

|---|---|---|---|

| 5–10 years | 50% to 65% | 5% to 25% | 0% to 10% |

| 3–5 years | 35% to 50% | 25% to 50% | 0% to 10% |

| 1–3 years | 20% to 35% | 25% to 65% | 0% to 10% |

| < 1 year | 5% to 20% | 25% to 65% | 0% to 10% |

Life Cycle Fund - 15 Year Tenure

| Years to maturity | Equity (%) | Debt (%) | Gold/Silver ETFs / ETCDs / InvITs (%) |

|---|---|---|---|

| 10–15 years | 65% to 80% | 5% to 25% | 0% to 10% |

| 5–10 years | 50% to 65% | 5% to 25% | 0% to 10% |

| 3–5 years | 35% to 50% | 25% to 50% | 0% to 10% |

| 1–3 years | 20% to 35% | 25% to 65% | 0% to 10% |

| < 1 year | 5% to 20% | 25% to 65% | 0% to 10% |

Life Cycle Fund - 20 Year Tenure

| Years to maturity | Equity (%) | Debt (%) | Gold/Silver ETFs / ETCDs / InvITs (%) |

|---|---|---|---|

| 15–20 years | 65–95% | 5–25% | 0–10% |

| 10–15 years | 65–80% | 5–25% | 0–10% |

| 5–10 years | 50–65% | 5–25% | 0–10% |

| 3–5 years | 35–50% | 25–50% | 0–10% |

| 1–3 years | 20–35% | 25–65% | 0–10% |

| < 1 year | 5–20% | 25–65% | 0–10% |

Life Cycle Fund - 25 Year Tenure

| Years to maturity | Equity (%) | Debt (%) | Gold/Silver ETFs / ETCDs / InvITs (%) |

|---|---|---|---|

| 15–25 years | 65–95% | 5–25% | 0–10% |

| 10–15 years | 65–80% | 5–25% | 0–10% |

| 5–10 years | 50–65% | 5–25% | 0–10% |

| 3–5 years | 35–50% | 25–50% | 0–10% |

| 1–3 years | 20–35% | 25–65% | 0–10% |

| < 1 year | 5–20% | 25–65% | 0–10% |

Life Cycle Fund - 30 Year Tenure

| Years to maturity | Equity (%) | Debt (%) | Gold/Silver ETFs / ETCDs / InvITs (%) |

|---|---|---|---|

| 15–30 years | 65–95% | 5–25% | 0–10% |

| 10–15 years | 65–80% | 5–25% | 0–10% |

| 5–10 years | 50–65% | 5–25% | 0–10% |

| 3–5 years | 35–50% | 25–50% | 0–10% |

| 1–3 years | 20–35% | 25–65% | 0–10% |

| < 1 year | 5–20% | 25–65% | 0–10% |

Zerodha Life Cycle Funds vs other options

Zerodha Life Cycle Fund vs index fund - A plain index fund holds a fixed exposure, say 100% large-cap equity, and stays there regardless of how close you are to your goal. The Zerodha Life Cycle Funds is built using index-tracking building blocks too, but it actively shifts the mix of those blocks along the glide path. You get discipline plus automatic asset allocation.

Zerodha Life Cycle Fund vs Balanced Advantage fund - A balanced advantage fund varies equity based on market valuations and is meant to run indefinitely. The Zerodha Life Cycle Fund varies equity based on time left to your goal and is built to wind down to a conservative stance by a specific year. One reacts to the market; the other follows a pre-defined schedule.

Zerodha Life Cycle Fund vs NPS - The NPS also offers age-based glide path options for retirement, but it is a retirement-specific, lock-in product with its own withdrawal and annuity rules. A Life Cycle Fund is an open-ended mutual fund you can use for any dated goal, retirement included, with the flexibility of a standard mutual fund structure.

Fixed maturity fund vs target date fund (Zerodha Life Cycle Fund) - These names get confused often. A fixed maturity fund is a debt fund that holds bonds to a set maturity date for predictable yield. A target date fund (such as the Zerodha Lifecycle Fund) is a multi-asset fund that glides across equity, debt, and commodities over time.

Do Zerodha Life Cycle Funds have an exit load?

Yes, and by design. A Life Cycle Fund works best when you stay invested for the full journey to your target year, so the structure carries an exit load that discourages early redemptions:

- 3% exit load if you exit within the first year of investment

- 2% exit load if you exit within two years

- 1% exit load if you exit within three years

- 0% exit load if you exit after three years

This is intentional. If you invest in the 2041 fund today and exit in 2028, the entire purpose of goal-based, glide-path investing is lost. Hence, there is an exit load to keep the strategy disciplined and your goal pointed in the same direction.

Are Zerodha Life Cycle Funds right for you?

A Zerodha Life Cycle Fund may suit you if you:

- Have a specific, long-term goal with a clear target year, such as retirement, a child's education, a home down payment, or any "fund for any other" objective

- Want a single-fund, set-and-forget solution that handles asset allocation and diversification automatically along a pre-defined glide path

- Would rather not monitor and rebalance a portfolio yourself every year

- Are disciplined enough to stay invested for the intended tenure

It may be less suitable if you prefer to actively manage your own asset allocation based on your reading of the market.

The honest question to ask is simple: do you actually rebalance your portfolio every year as your goal approaches? If the answer is "rarely", a Life Cycle Fund closes the gap between intention and execution.

The Bottom Line

Target date investing has anchored retirement savings across the world for decades. With the Zerodha Life Cycle Funds, India now has its own version: a rule-based, goal-first mutual funds that grow up alongside your goal and shift from growth-oriented allocation to conservative assets on a defined schedule, so you don't have to.

* Please note that:

- Exposure to Gold ETFs shall be at a maximum of 5% of the AUM.

- Exposure in debt instruments shall be limited to AA & above rated instruments with residual maturity less than the target maturity of the schemes.

- This allocation schedule is prepared solely for the purpose of representing the indicative glide path of the scheme's asset allocation. The allocation ranges indicated herein are derived from, and must be read in conjunction with, the asset allocation table as set out in the Scheme Information Document (SID) of Zerodha Life Cycle Fund 2036 & Zerodha Life Cycle Fund 2041 .

- The SID of Zerodha Life Cycle Fund 2036 & Zerodha Life Cycle Fund 2041 is the definitive and governing document for all purposes. In the event of any conflict, ambiguity, or inconsistency between this allocation schedule and the SID, the asset allocation table as specified in the SID shall prevail in all respects. This allocation table does not, in any manner, amend, modify, or supersede the SID or any other scheme-related document.

- Investors are advised to refer to the SID and the Key Information Memorandum (KIM) of Zerodha Life Cycle Fund 2036 & Zerodha Life Cycle Fund 2041 for complete details on asset allocation, investment objectives, risk factors, and other scheme-specific information before making any investment decision.

- The exposure mentioned above is only an intended illustration and the actual exposure may vary depending on various factors.

Disclaimer - Please note that this article or document has been prepared on the basis of internal data/ publicly available information and other sources believed to be reliable. The information contained in this article or document is for general purposes only and not a complete disclosure of every material fact. It should not be construed as investment advice to any party in any manner. The article does not warrant the completeness or accuracy of the information and disclaims all liabilities, losses and damages arising out of the use of this information. Readers shall be fully liable/responsible for any decision taken on the basis of this article or document.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Published on Jun 19th 2026